Bill 26 – LNG Income Tax Amendment Act

On Wednesday, April 15 I rose to speak to Bill 26, Liquefied Natural Gas Income Tax Amendment Act 2015. Bill 26 introduces 109 pages of amendments to Bill 6, the Liquefied Natural Gas Income Tax Act that was introduced and subsequently granted Royal Assent in the 2014 Fall session.

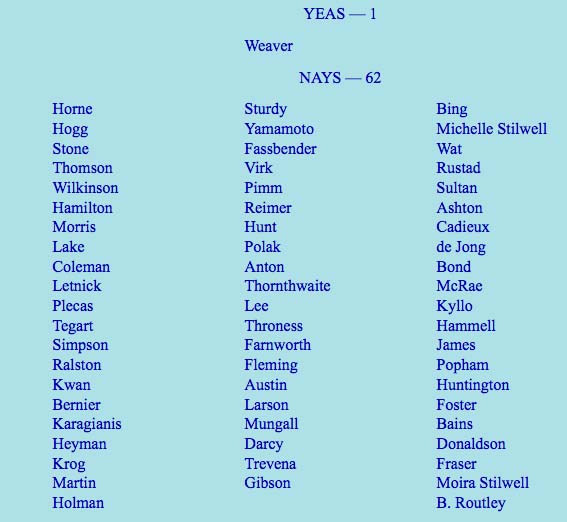

In the fall I stood alone in the house opposing Bill 6. During second reading of the bill I spoke out against it. I described it as a “generational sellout” that was incomplete and full of loopholes. I noted that in a desperate attempt to fulfill outrageous election promises, the BC Government did what it could to give away our natural resources with little, if any, hope of receiving LNG tax revenue for many, many years to come. Every single member of the legislature apart from me voted in support of the bill at second writing (see the image to the right).

In the fall I stood alone in the house opposing Bill 6. During second reading of the bill I spoke out against it. I described it as a “generational sellout” that was incomplete and full of loopholes. I noted that in a desperate attempt to fulfill outrageous election promises, the BC Government did what it could to give away our natural resources with little, if any, hope of receiving LNG tax revenue for many, many years to come. Every single member of the legislature apart from me voted in support of the bill at second writing (see the image to the right).

During the committee stage for the bill after 2nd reading, I identified a number of potential loopholes that could be exploited by LNG companies to further reduce the already meager amount of tax that they would pay to BC. And then, at third reading, I moved an amendment that would have sent Bill 6 to the Select Standing Committee on Parliamentary Reform, Ethical Conduct, Standing Orders and Private Bills, so that British Columbians could get answers to unresolved questions about the government’s LNG promises. The bill would have benefitted from a more thoughtful analysis by the Select Standing Committee. Third parties could be brought in for consultation, including the public, including First Nations and including the companies involved.

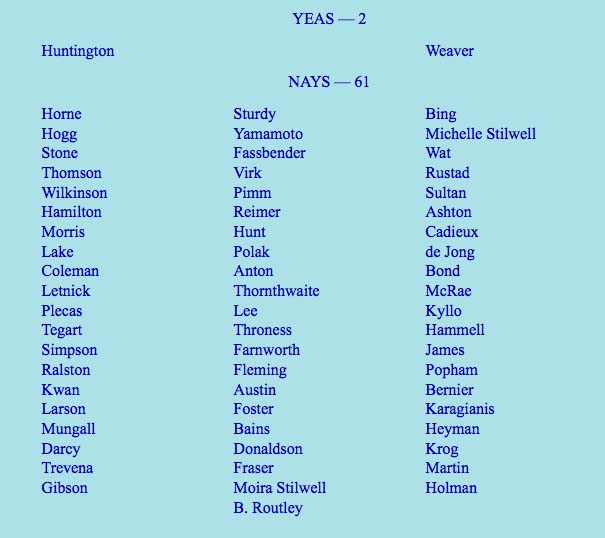

When it came to the vote, only independent MLA Vicky Huntington (Delta South) stood with me in the Chamber in calling for more time. The official opposition and the government voted together. It was truly remarkable to witness the opposition collectively stand in favour of this bill. So many of them had offered scathing condemnations of it during second reading.

When it came to the vote, only independent MLA Vicky Huntington (Delta South) stood with me in the Chamber in calling for more time. The official opposition and the government voted together. It was truly remarkable to witness the opposition collectively stand in favour of this bill. So many of them had offered scathing condemnations of it during second reading.

Imagine my surprise when the 109 page LNG Income Tax Amendment Act (Bill 26) was brought in for debate during this session. As I outline in my speech below, the actions taken by this Legislature in the fall, I believe firmly, were a dereliction of our duty. As MLAs, we should have explored the incomplete bill in greater detail. That could and should have been accomplished by sending it to the Select Standing Committee.

Bill 26 puts me in a quandary. I was fundamentally opposed to passing Bill 6 in the Fall. Yet the BC Liberals and the BC NDP voted to move it through quickly and so it is now law in British Columbia. Many of the objections I raised concerning the incompleteness of Bill 6, including the many loopholes and lack of completeness, were addressed in the LNG Income Tax Amendment Act (Bill 26). It is important that we fix bad law.

But at the same time, Bill 26 introduces an unacceptable revision to section 56. Now the minister is granted the power to use regulation to allow corporations involved in the LNG industry to use their natural gas tax credit to pay an 8 percent corporate tax instead of 11 percent. Obviously the government is so desperate to try and land an LNG industry that it is sweetening the pot still further. Back in the fall, when I put an amendment to send this to committee, I specifically stated in speaking to that amendment that one of the reasons this had to go to committee was because “I would have wished to explore, in particular the one-half percent natural gas tax credit.”

Section 56 represents one section of the bill that I will propose an amendment to during committee stage. I will propose to revert it back to its original fall version.

The BC NDP took a different approach. They too opposed changes to section 56. But instead of waiting to committee stage they decided to vote against the 2nd reading of the bill (which means all the Bill 6 loopholes would be left in place).

Below are the video and text of my speech.

Second Reading Speech Video

Second Reading Speech

A. Weaver: I find it, frankly, deeply troubling that we’re here debating Bill 26, LNG Income Tax Amendment Act. This is a 109-page act which is designed to amend an 87-page act — that is, Bill 6, which was introduced back in the fall. Bill 6, as you will recall, hon. Speaker, was the Liquefied Natural Gas Income Tax Act.

You will recall that in third reading of Bill 6, I moved a motion. I moved a motion to send the LNG Income Tax Act to the Select Standing Committee on Parliamentary Reform, Ethical Conduct, Standing Orders and Private Bills for further review. The reason why I did that was because Bill 6 was incomplete. It was full of loopholes so big you could drive a bus through.

Let me read some of the concerns I had. The reason why I would like to do that is to point out that quite a number of these concerns have been addressed in this, the amendment act, this 109-page act — bigger than the original act.

In the fall, when I moved an amendment at third reading to send this to committee, I stated the following.

“There have been questions that would benefit exploration at committee stage. In particular, there are questions on revenue projections, the modelling, the assumptions into the modelling that have not been forthcoming and transparent in terms of us as a Legislature being able to assess this legislation.

“There’s section 32(c)” of Bill 6. “There are issues that came up…with respect to a loophole for earned credits that could be sold by a company, the income from that not being claimed as taxable, yet the person purchasing it can claim the income as a deduction.”

There were questions about section 46, with respect to the rate being left out. We never got guidance as to what the rate and the formula there was.

There were questions on section 47 regarding “a potential LNG loophole for tax avoidance through capital acquisitions and leaving the 1.5 percent net LNG tax rate for significant times.”

There were questions on section 122 with respect to the polluter-gets-paid instead of a polluter-pays model.

There were questions on section 172 that we did not have as much time as I would have liked to explore, in particular that one-half percent natural gas tax credit. Let me reiterate that. Back in the fall, when I put an amendment to send this to committee, I specifically stated in speaking to that amendment that one of the reasons this had to go to committee was because “I would have wished to explore, in particular the one-half percent natural gas tax credit.” Well, as we will discuss later in my speech here, we do have more details about that one-half percent tax credit.

I would have thought in the fall that this was such an important piece of legislation that government would have wanted to send this to committee to actually gain the insight of British Columbians, of First Nations, of industry from across the province. Instead, with the exception of the member for Delta South, every member in this Legislature stood and voted against sending this to committee, to rush this bill through when it wasn’t ready.

Today we stand here to debate Bill 26, the Liquefied Natural Gas Income Tax Amendment Act, a full 109 pages, compared to the 87-page act which was incomplete and introduced in the fall. This is troubling. This is very troubling. It, frankly, disturbs me that we have to be in this position here today.

Let me emphasize that the changes made in this bill are important. They’re important, and I’m in a quandary. They’re important because I stood passionately and spoke against the introduction of Bill 6 in the fall. But I recognize that we have passed Bill 6. Bill 6 has now received royal assent and is a matter of law within British Columbia. Bill 6 is incomplete. We cannot conduct business in the province of British Columbia with Bill 6 standing before us now. We either need to repeal it or we need to pass some form of legislation to fill those loopholes.

Let me address some of that. In essence, my own view is that this bill closes quite a number of those massive loopholes that I referred to earlier. In particular, if I could read the…. I have so many notes here. I’ll find it in a minute. Let me say it provides greater clarity on the administrative requirements, bankruptcy and insolvency issues and debt forgiveness rules. It sets requirements for registration, for filing tax returns and for paying and refunding taxes. It establishes penalties for failing to meet the requirements of the act.

Most importantly, it introduces section 124.412, which is the anti-avoidance rule, which was so critical in my criticism back in the fall, that there were so many loopholes that companies could avoid paying taxes even though they were hardly paying any taxes in the first place. This anti-avoidance rule introduction is critical legislation that needs to have been in place and should have been in place in the fall and should have been discussed and raised in committee, had we passed this legislation and sent it to committee. Instead, here it is now in the 109-page liquefied natural gas amendment act.

There are essential aspects in this bill for the tax regime. Without them, LNG income tax payers could avoid paying a significant amount of the tax because of the massive loopholes and others that I discussed earlier.

The real question is how the LNG Income Tax Act got passed last fall without any of these very basic provisions laid out for us to discuss, number one. Two, not sending this to committee so that we could have an opportunity to discuss it is deeply, deeply troubling. Frankly, in my view, this has been an abdication of the responsibility on behalf of this Legislature to do due diligence on the legislation that was tabled and brought to us. It doesn’t end there.

Here I do agree entirely with the official opposition — that is, with the concern they raised, which I agree with, concerning the problematic natural gas tax credit. Before I come to that, I think it’s important to set the context.

What is the context? Why is it now that in section 56 we essentially allow the minister, through regulation and in perpetuity, to allow corporations involved in the LNG industry to use this natural gas tax credit to pay 8 percent instead of 11 percent?

Let me tell you a little bit why we’re where we are. And this isn’t new. For two years now I’ve been saying the same thing. British Columbia’s hype of hope and wealth and prosperity for one and all from a hypothetical LNG industry was nothing more than a message of hope wrapped in hyperbole. The promises of 100,000 jobs, a $100 billion prosperity fund, a $1 trillion increase to GDP, debt-free B.C., no PST, thriving schools and hospitals and on and on were nothing more than a pipe dream.

The global markets, the economics, did not support these statements in the fall of 2012. They do not support these statements now. This is the reason why we’re seeing this natural gas tax credit — essentially, yet another generational sellout on top of the existing generational sellout — being brought to us for approval today.

What has happened since 2012 was entirely predictable — entirely predictable — given the fact that we are not the only ones in the world who have discovered horizontal fracking technology. Our shale gas reserves pale in comparison to others. We have massive reserves in Australia, in Russia, even in China, in the United States, in Iran, in Qatar. I could go on and on. There is shale gas all over the world. Yet somehow B.C. thinks that it, and it alone, is going to fill Asian markets with natural gas.

This is what happened. I’m reading here from a Reuters piece published on December 11, 2014. The title of that says this: “Asian LNG Prices Seen Falling by up to 30 Percent in 2015.” Well, they’re talking about LNG prices falling 30 percent in 2014. But in fact, they talk here about things like if brent crude trades at $85 next year, the price could be $12.60 per million Btu. It continues on that it could drop still further and further. If brent trades for $70 a barrel — $70 a barrel; hmm, lot of oil companies out there right now are looking for $70 a barrel — the price of low-sulphur oil will cap LNG spot prices at — guess what — $10.50 per million Btu.

I’ll repeat that. If brent trades at $70 a barrel — it doesn’t matter that we’re trading at $50 a barrel now — this Reuters article is quoting Wood Mackenzie’s Thompson as saying that LNG spot prices will be capped at $10.50 per million Btu. That makes sense.

Russia has just entered into long-term 30-year contracts at below that price. Yet British Columbia thinks that somehow companies will invest tens of billions of dollars to transport liquefied natural gas from our coast across the ocean, when it costs $7 to $8 per million Btu to do that. They’re going to have to pull this out of the ground at negative prices.

That is why we have this LNG tax legislation before us, because it introduces so many giveaways that, essentially, we avoid paying tax to British Columbians, and we give away a natural resource. Well, we try to. This is still not coming.

I reiterate, and I say it one last time. If brent trades at $70 a barrel, the price of low-sulphur oil will cap LNG spot prices at about $10.50 per million Btu.

It doesn’t end there. What other things have happened to cause this desperate Hail Mary pass of hope after the previous Hail Mary pass of hope was caught? They didn’t win the game. We thought they did, but they didn’t, because they can’t land this.

Let’s see what else has happened. I’ll read to you from a Toronto Star article entitled “Shell-BG Deal Could Dampen B.C. LNG Projects.” Well, that’s a surprise. I thought we were going to have Shell and BG and three others up and running by…. Well, one of them should have been this year, maybe a couple by next year.

The Shell and BG amalgamation is troubling. Why is that? Because they have…. Let me read here. British Gas, BG, has liquefication plants in Australia, Egypt, Trinidad and Tobago, and another being developed in Louisiana.

Shell has LNG operations under construction — not planned, under construction — in Russia, Qatar and Australia. We now have dropping demand. We have the amalgamation of two major players in the liquefied natural gas world with projects under construction. B.C. is not a player here. We can say goodbye to those companies.

Why would anyone invest in British Columbia right now? Why would anyone invest? Because they would need a supply gap. These companies don’t buy to fill spot prices. They buy to make long-term investments to fill in supply gaps down the road. Petronas had a supply gap — 2018-2019. They’ve deferred their investment decision, deferred it again and again. Do we really think Petronas is going to make a final investment decision to go ahead to meet a 2018-2019 supply gap? I don’t think so. They may be back in the mid-2020s, where another supply gap emerges there. But for the short term, this is nothing but hope.

Frankly, it’s irresponsible to put our entire provincial economy, to retool our education systems, to essentially send to business a message, a singular message, that if you want to come to British Columbia to do business in our province, you’ve got to hang your hat on LNG, an industry that doesn’t exist now, but we hope maybe someday will exist. What we’ll do for you, hypothetically, is retrain our education system. We’ll do whatever you want. We’ll create a natural gas credit, which is 1/2 percent plus some random number to bring it down to 8 percent — your corporate income tax that you pay.

Here’s another article, published on April 5. This one’s important, because this government has pointed out for us many, many times how proud they are to get the triple-A credit rating from Moody’s. Well, low and behold, here’s the title: “Moody’s Puts a Damper on B.C.’s LNG Dreams.” I’ll say it again. “Moody’s Puts a Damper on B.C.’s LNG Dreams” — published in the Canadian Press and syndicated across our beautiful country.

Meanwhile, what’s actually happening in the world? Well, we don’t have to go very far. Let’s go to Bloomberg Business today — not tomorrow, not yesterday but today’s Bloomberg Business newspaper. Let me quote the title article. It says this: “Fossil Fuels Just Lost the Race Against Renewables.”

Why is that the case? Because, around the world, people recognize that there are stranded carbon assets in the ground that cannot be extracted. The existing plans and development to extract those resources that are there are already meeting existing demand down the road, so there are no supply gaps.

Instead, places like China, Russia, Europe, Australia and America, whose emissions dropped last year, are going all into the renewable clean tech sector, a sector that British Columbia used to be a leader in.

Now this government is saying to British Columbians: “If you want to be a leader in an economy in B.C., forget everything else. Let’s go LNG.”

This article, which I recommend that all read, entitled “Fossil Fuels Just Lost the Race Against Renewables,” is published today in Bloomberg Business. There are actually some lovely charts and graphs in there too. It’s not just some person writing their opinion. It’s actually an analysis with graphs, bar charts. It’s quite interesting to read, because they’re saying what I have been saying for two years — that this is nothing but hyperbole.

This brings me to the most serious aspect of this bill again, and that is the natural gas tax credit. Under this tax credit, an LNG taxpayer can decrease their corporate income tax from 11 percent to 8 percent by claiming credits for the cost of natural gas. Under the old version from last fall, they could only claim 0.5 percent of their natural gas costs.

I agree with the opposition. This is simply unacceptable. This should’ve been brought in, in the fall. However, my approach to deal with this is to amend this at third reading and offer this Legislature an amendment to refer us back to the fall legislation, which had this fixed value of 0.5 percent — as opposed to voting against this at second reading.

Under the new version an LNG taxpayer can claim that amount as well as an additional prescribed amount that is to be set by the Lieutenant-Governor-in-Council. It could be 0.5 percent or, given that that brent crude drop is going to cap LNG prices, you might as well make it 0.5 percent plus minister’s 2½ percent to make it 3 percent to drop the corporate tax down to 8 percent. We weren’t told that in the fall, and it behooves us in this House to amend this, to take it back to what was given us in the fall with a straight face by this government that this number would be a half-percent.

What’s worse here is that if is a taxpayer claims for credits than they can use in a year, those additional tax credits will carry over to future years, which means that if the prescribed rate is high enough, a company could end up paying 8 percent corporate income tax in perpetuity. Yet another loophole is brought in here, and based on the changes that are being made, it’s is hard to imagine any other intention.

Clearly, the government did not think that 0.5 percent of a taxpayer’s natural gas costs was sufficient enough to lower their corporate income tax rate to 8 percent. It was not a sufficient enough gift — a piece of candy — to give to the LNG industry that they introduced greater cuts because the industry is not coming here. What is next? Are we going to have to promise them a free workforce? Are we going to promise them that they pay no tax? They’re not coming, even as we introduce this generational sellout of Bill 6, amended through Bill 26.

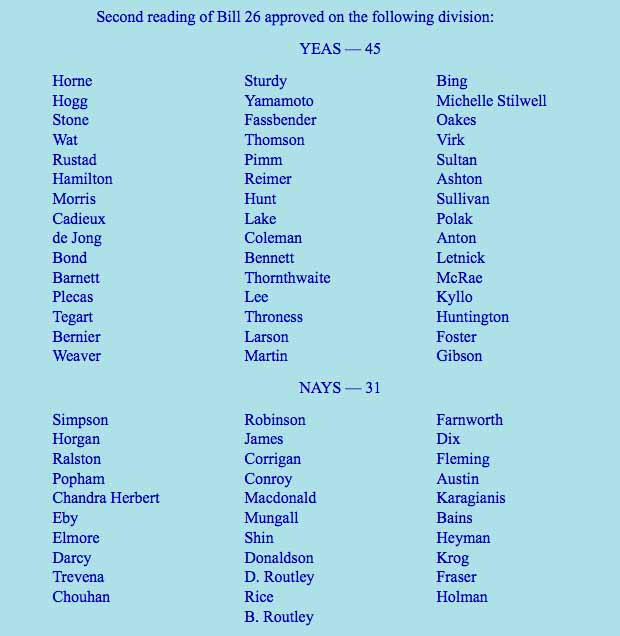

Let me discuss now the quandary we find ourselves in, because this is important. This bill puts us, all of the members in this Legislature, in a quandary, in a very difficult position. Last fall the government and the official opposition together passed the LNG Income Tax Act prematurely. At second reading I was the only member of this Legislature to stand in opposition to the generational sellout embodied in Bill 6. I would have argued that this should never have happened. But now we are debating an amendment that is longer than the actual act, and this amendment actually dramatically changes the original act.

The problem here we face is…. I tried in the fall to put this to committee, because it was clear that there were so many loopholes in this bill — loopholes, as I described, that you could drive a bus through. I was voted down by every member in this House except my dear friend from the riding of Delta South, who also recognized that while her position was that it was important to move forward with an LNG tax regime, we could not do so at this time in light of lacking information before us, and so sending this to committee was critical.

The problem now is that we’re not really able to debate the merits of the original act. We are debating the amendment act, with the original act now standing as a matter of law before all British Columbians. So I’m in a quandary, as I’m sure others are, and I say it again very clearly that I believe that the LNG Income Tax Act, Bill 6, should be repealed. It should never have passed.

Here we are today with a government not willing to do so, a government instead amending — amendments that I support — many of the loopholes in the previous act but introducing section 56, which, to me, is critically flawed in actually, essentially, giving regulation to the minister to allow him or her to grant 3 percent income tax cuts to LNG corporations in perpetuity.

As I said, the actions taken by this Legislature in the fall, I believe firmly, were an abdication of our duty, a dereliction of duty. As MLAs, we should have explored that in greater detail.

I am grateful to the minister for allowing me to be briefed by his staff, a briefing that I was able to probe many of the loopholes that I raised earlier and find that many of them have been addressed. I was satisfied with the answers I got, and I was pleased by the level of detail provided.

Clearly, I’m unhappy with section 56. While I support the amendments, I will not support section 56. But I will do that at the committee stage through the introduction of an amendment if the official opposition does not.

The Vote

Comments are closed.

Latest Posts

Recent Comments

- on The Paris Agreement is in trouble: UNFCCC needs to ratchet up their climate efforts

- on The Paris Agreement is in trouble: UNFCCC needs to ratchet up their climate efforts

- on How can BC’s environmental organizations be more effective?

- on How can BC’s environmental organizations be more effective?

- on How can BC’s environmental organizations be more effective?