Affordability

Initial response to the BC NDP Speech from the Throne

The 4th session of the 41st parliament opened today with the Speech from the Throne. As noted in our accompanying press release (reproduced below), while we are pleased that the Throne Speech recognized the important work that has been achieved on the priority initiatives outlined in the Confidence and Supply Agreement between the B.C. Greens and the BC NDP, we are concerned by the apparent lack of broader vision outlined in this speech.

I’ll be responding to the Speech from the Throne tomorrow and look forward to expanding on these initial comments then.

Media Release

B.C. Green Caucus responds to the Throne Speech

For immediate release

February 12, 2019

VICTORIA, B.C. – The B.C. Green Caucus responded today to the 2019 Speech from the Throne.

“We are pleased the Throne Speech recognized the important work that has been achieved on the priority initiatives outlined in the Confidence and Supply Agreement between the B.C. Greens and the BC NDP,” said Andrew Weaver, leader of the B.C. Green Party. “In particular we are glad that it highlighted the importance of CleanBC as British Columbia responds to the challenges and opportunities offered by climate change.

“However, we are concerned by the apparent lack of broader vision outlined in this speech,” said Weaver. “Trying to be all things to all people leads to contradictory legislation and puts the focus on short term policy instead of long term outcomes.

“Although we are pleased to see CleanBC highlighted, the government’s praising of LNG immediately undercut its point,” Weaver added. “Economic opportunity and ecological stewardship are not mutually exclusive, but this government is focusing on short term investments that will exacerbate climate change, impacting our economy, environment, and the wellbeing of our communities for years to come.”

This year’s Throne Speech referenced important investments in childcare and education, addressing affordability, and improving transportation services. These issues are all important to British Columbians, but issues that were overlooked in the speech underscored the government’s focus on short-term gains rather than establishing a long-term vision for British Columbia.

“British Columbians need to be able to trust that their government is prepared for the future. Investing in education and childcare is central to a healthy and prosperous future for BC,” said MLA Sonia Furstenau. “This government has taken important steps towards improving the services that children and families depend on, yet there was no vision articulated for how to create immediate solutions to the urgent issue of the over-representation of Indigenous children in government care.”

British Columbia’s ecology is critical to the identity and economy of our province. The government must act as a steward of sustainability to ensure the long-term well being of our province.

“Wild salmon have immense cultural, economic, and ecological value for British Columbians. I am glad that this was recognized in the Speech from the Throne,” said MLA Olsen, whose advocacy on wild salmon led to the establishment of the Wild Salmon Advisory Council last year. “With the work of the Wild Salmon Advisory Council now complete, I expect government to get to work and actually start implementing its recommendations – starting with habitat protection and restoration.”

The B.C. Green Caucus anticipates that CleanBC will be fully funded in the government’s budget next week and will continue to hold government to account to ensure that a long term vision is articulated for British Columbians.

-30-

Media contact

Macon McGinley, Press Secretary

+1 250-882-6187 |macon.mcginley@leg.bc.ca

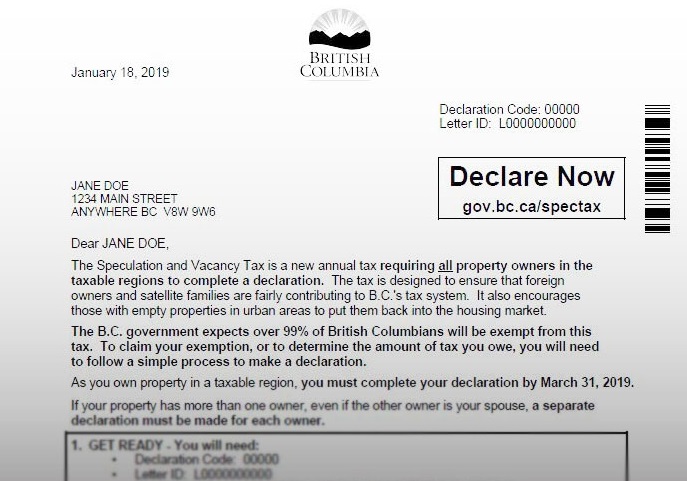

On the botched rollout of BC NDP’s Speculation and Vacancy Tax

Residents across the Lower Mainland, the Capital Regional District, Nanaimo and  Kelowna/West Kelowna are beginning to receive letters from the BC NDP government concerning the Speculation and Vacancy Tax. To the surprise of most, every property owner registered on title will have to fill in a declaration to claim exemption from the tax. Widespread concern has emerged that this form of “negative billing” will lead to myriad problems. I agree.

Kelowna/West Kelowna are beginning to receive letters from the BC NDP government concerning the Speculation and Vacancy Tax. To the surprise of most, every property owner registered on title will have to fill in a declaration to claim exemption from the tax. Widespread concern has emerged that this form of “negative billing” will lead to myriad problems. I agree.

Anyone following BC politics will know that the BC NDP’s Speculation and Vacancy Tax has been, and continues to be, extremely controversial. Shortly after signalling, in February 2018, their intent to introduce tax legislation later in the Fall, it became abundantly clear to me that the BC NDP hadn’t thought the tax measure through. I was very critical of the lack of details and the fact that the tax’s interpretation by the Minister of Finance seemed to be changing on a near daily basis.

I was unconvinced that the BC NDP knew what outcome they were trying to achieve with their tax measure. I arranged for briefings; I met with the Minister of Finance where I outlined my many concerns; I posed questions to her in the legislature (e.g. in Question Period); I met with numerous stakeholders. And I personally responded to many hundreds of emails from around British Columbia.

The BC Green efforts started to pay off. In late March government released a second intentions paper outlining a series of thresholds, exemptions and refinements to the geography of affected areas. While I was supportive of these changes, there was still much work that needed to be done.

And so I arranged for more briefings; I again met with the Minister of Finance to once more outline my ongoing concerns; I posed questions to her in the legislature (e.g in Budget Estimates); I met with numerous other stakeholders. And I personally responded to many more hundreds of emails from around British Columbia.

On June 27 I published online an email that I had started to send out to people about my ongoing concerns over the Speculation Tax. Over the summer I once more arranged for more briefings; I met with the Minister of Finance; I met with numerous other stakeholders. And I personally responded to many more hundreds of emails from around British Columbia.

When the BC NDP finally introduced Bill 45: Budget Measures Implementation (Speculation and Vacancy Tax) on October 16, 2018, I acknowledged that they’d gone a long way towards addressing many of the unforeseen negative consequences that I’d raised with them. Yet there were still several key aspects of the bill that caused my BC Green Caucus colleagues and I to reiterate our ongoing concerns.

Prior to the introduction of the Bill, the BC NDP told our caucus that they viewed Bill 45 as a confidence measure. They argued that it arose from a flagship “budgetary policy” announced as part of the 2018 budget. Our position was that our Confidence and Supply Agreement was very clear:

“While individual bills, including budget bills, will not be treated or designated as matters of confidence, the overall budgetary policy of the Government, including moving to the committee of supply, will be treated as matters of confidence“

As you might imagine, a number of (at times difficult) meetings followed with the BC NDP. Concurrently, my caucus colleagues and I united behind the notion that the only way the BC NDP would secure our collective votes was if, and only if, they supported three further amendments (which were subsequently drafted by Legislative Drafters). These amendments ensured that:

- Mayors from affected municipalities would be part of an annual review process with the Minister of Finance that required the Minister to provide metrics that justified keeping the speculation tax in place in their community;

- revenue raised by the tax would be used for housing initiatives within the region it came from;

- the speculation and vacancy tax rate for all Canadians was the same – this brought the rate for non BC-resident Canadians down from 2.0% to 0.5%.

The amended Speculation and Vacancy tax bill eventually passed in the BC Legislature, but not before I was able to ensure that the Minister provide further clarification on record as to its intent.

At this point it’s important to note that the BC Greens take the enormous responsibility British Columbians have granted us very seriously. Our role in the BC Legislature is to ensure stability, yet accountability. And we did just that. We ensured that the BC NDP government did not fall in their declared confidence measure while at the same time working tirelessly to ensure that many of the unforeseen consequences of the poorly-thought-through Speculation and Vacancy Tax were mitigated.

Several times in our meetings with the Minister and/or her staff, or during the briefings with the Ministry, I raised concerns and questions about government’s proposed negative billing during the implementation of the tax (the BC Liberals were apparently asleep at the wheel and didn’t realize this was involved with its implementation). I suggested that some people might get confused and pay the tax even though they didn’t need to. My concerns were dismissed as I was told that the process was going to be easy and transparent, like what is already in place for people claiming the Homeowner Grant.

Sadly, this has not turned out to be the case and the processes to claim a Homeowner Grant and declare an exemption from the Speculation and Vacancy Tax remain separate. And so, while I am not surprised by the public reaction to the rollout of this tax, I am surprised that the BC NDP hadn’t anticipated this.

The BC Greens remain of the opinion that the BC NDP’s Speculation and Vacancy tax is bad public policy.

We believe that a better way forward would be to enable all local governments (not just Vancouver) to introduce vacancy taxes if they felt it was in their community’s interest. At the same time, a speculation tax could be applied exclusively to properties owned by offshore individuals and entities, the Bare Trust loophole could be closed as was done in Ontario, and a flipping tax could be applied when the same property is sold multiple times in a short time period.

We believe that a better way forward would be to enable all local governments (not just Vancouver) to introduce vacancy taxes if they felt it was in their community’s interest. At the same time, a speculation tax could be applied exclusively to properties owned by offshore individuals and entities, the Bare Trust loophole could be closed as was done in Ontario, and a flipping tax could be applied when the same property is sold multiple times in a short time period.

The BC Greens understand the importance of tempering exuberance in the out of control housing market. In fact, we specifically called for a New Zealand-style ban on off-shore purchases as per our call for bold action. We also outlined numerous other measures that could be implemented.

Moving forward, our caucus will continue to ensure stability, transparency and accountability in the BC Legislature.

Clarifying the intent of the Speculation and Vacancy Tax

Over the course of this week, Bill 45 – 2018: Budget Measures Implementation (Speculation and Vacancy Tax) was being debated during committee stage. During this stage, the BC Green amendments were all approved.

Those who have been following this file will know that I have spent an enormous amount of time on it over the last year. When this tax was first introduced in the February budget it was, in my view, poorly thought through and seemed to be an overly blunt instrument that did not effectively target its key overarching goal of dealing with speculation, affordability and vacancy rates. As I noted in March,

“The Speculation Tax … need[s] the introduction of legislation prior to [it] taking effect. Such legislation is expected in the fall. Fortunately we have time to pressure government to fix the problems embedded in their poorly thought out approach to deal with speculation.”

The bill that was ultimately introduced in October was certainly tempered from that which was originally offered through the first intention paper released by the government earlier this year. Many of the concerns we brought to government had been addressed. While it is still not the approach I would have taken, our amendments improved the bill further and will mitigate many of the key issues I had identified.

During committee stage I rose to ask questions and speak to amendments far too many times to reproduce all the Hansard records. However, I took the opportunity to raise a few specific, yet illustrative examples that were brought to my attention from the myriad emails we received and responded to. Below I reproduce the video and text of my exchange with the Minister on these specific examples.

What’s important is that if you have specific questions as to whether or not the speculation and vacancy tax applies to a property you may own, please note that details information is available at gov.bc.ca/speculationtax. Alternatively, you can email: spectaxinfo@gov.bc.ca or phone 1-833-554-2323.

The bill eventually passed on Thursday.

Videos of Exchanges

| Video 1 | Video 2 | |

| Video 3 | Video 4 | |

| Video 5 | Video 6 |

Text of Exchanges

Example 1 (Video 1): Belcarra – only accessible by air or water

A. Weaver: I enjoy this line of questioning. I think it’s very important to get clarification on the intent of the legislation before us. I have three questions on the definition of “specified area” in this section.

The first is with respect to item (l) in specified area. It refers there…. It just says: “…an island, if any, within an area referred to in paragraphs (a) to (j), if the island is usually accessible only by air or water throughout a calendar year.”

The first question is: why was the term island used there as opposed to a general area within these (a) to (j) that are generally accessible only by air or water? I’ll come to a specific example. Within the broader area, there may be, in fact, regions that are only accessible by air or water, even though they lie within the areas covered in (a) to (i).

Hon. C. James: As the member knows, the exclusion, when we looked at how to refine the geographic areas and looked at, as I mentioned in our discussion yesterday, the issue of how you make sure that most vacation homes are excluded…. We took a look at a number of different options, and one of them was to look at refining the geographic area.

That’s why we’ve said that we exclude islands that aren’t accessible, or that only are accessible by air and water — to be able to address those areas that, again, are difficult for commuting and, therefore, in most cases, are not people who are commuting and buying second homes. They’re mainly vacation homes, which is why we’ve listed it under (l) in that way.

A. Weaver: I very much appreciate the answer and the intent of actually including islands.

Why I raised it is that I heard from a resident of Belcarra, which, as the minister will know, is a lovely piece of the Lower Mainland across from Deep Cove. This person actually owns a property in Belcarra that is not accessible by road and is only accessible by air or water.

It seems that the intent of the legislation was to actually ensure that we’re dealing with urban areas where there are issues of commuting and issues of a rental market that’s being at ease here. Clearly, I would have thought the intent of this legislation would not have been to include somebody with a home in Belcarra that is not accessible by road and only accessible by air or water.

My question to the minister is: to what extent does a person who lives in the region — in one of these designated, prescribed areas — have an ability to actually get government to recognize that the spirit and intent of this legislation probably wasn’t meant to apply to an area which is only accessible by air and water but happens to be in one of these geographical regions?

Is there a mechanism that this person, recognizing the spirit of the minister’s previous statement, could go forward to actually determine whether or not this really is appropriate and they were meant to be covered under the government’s intentions?

Hon. C. James: We did specifically look at Belcarra. Part of the logic was, again, looking at the commuting distance. In fact, the commuting distance from Belcarra…. It’s a very short commute to downtown Vancouver. In fact, it’s a shorter commute from others that go from the Fraser Valley or from other distances — North Vancouver, for example. Five minutes away.

It is a municipality though, and I think this is important. As the member asked: what opportunities are there for discussion around these issues? Belcarra, in fact, is a municipality. I met with the Belcarra folks at UBCM. They will have the opportunity, in an informal setting anytime, but in a very formal setting, as the member knows, with the amendment coming forward, to have an opportunity to be able to argue either the strength or weakness of having the municipality included.

The Chair: Noting the time, we’ll take one more question.

A. Weaver: On this topic. I have one more question after this. I don’t know whether….

The Chair: Of course. As long as the minister can address the questions, we’ll do them.

A. Weaver: It’s just to follow up on that further, very briefly.

I’m not talking about the entire region of Belcarra. But within the broader section of Belcarra, there are parts of Belcarra — properties that happen to have cabins on them — that are only accessible by water or air. Therein lies the issue here.

It may be that the municipality itself meets the intent that the minister sought of a commutable distance. However, it’s not a commutable distance for some aspects of this municipality that extend into areas that are actually not an island but are only accessible by air or water.

Again, my question for a specific individual within this broader municipality: is there a mechanism for that individual to seek an exemption, as per my earlier remarks?

Hon. C. James: Thank you for the question, again. I think we did, in fact, look at the commuting time from some of the areas that were only accessible by boat — five to eight minutes to get to the Lower Mainland — so there are commuting pieces there. There aren’t opportunities other than, obviously, coming forward and raising the issue.

There aren’t opportunities built into the legislation, but I expect that people will have the opportunity to argue that changes should be made, if changes are going to be the made to the tax, including the mayor, who, I’m sure, will represent all the members of the municipality.

Example 2 (Video 1): Mudge Island and Nanaimo

A. Weaver: My final question is very brief. It’s from another concerned couple who approached me. I’m just giving a sampling of them because they illustrate the variety of concerns out there. I believe I know the answer, but I’d like to get confirmation from the minister.

The couple lives on Mudge Island in the Nanaimo regional district. They’re concerned that the tax could afford them and that it could kill the property values on Mudge Island. Can the minister confirm — they live in their home full-time on Mudge Island — that Mudge Island is not included in the regions that are prescribed under the specified areas?

Hon. C. James: I think the first piece that the member raised is primary residence. If it’s a primary residence and they live there full-time, then they aren’t captured. It isn’t captured. It’s only second or third homes. But Mudge Island is not captured by the speculation tax as well.

Noting the time, hon. Chair, I move that we rise, report progress and seek leave to sit again.

Example 3 (Video 2): Owned by couple in different countries

A. Weaver: I wasn’t planning to step up here and ask this question, but I’m very pleased the member for Prince George–Valemount did address this specific issue that I was going to raise under section 8.

I’d just like to ask a follow-up on this. I have the same letter, and we’ve been in communication with the same person. A good example that highlights some of the complexity of the application of this legislation — this particular case. The partnership is a partnership where one of the…. They’re not formally married. They’re living separately. One lives in a jurisdiction other than Canada. That person owns 20 percent ownership in the property that is the condo that is owned by the other partner.

So my question to this: given the fact that this couple are not formally married, if the person living in the foreign jurisdiction were able to rent back to her partner here in Canada, would that exempt her from the speculation tax? Yes or no?

They are not married, according to the court of law in Canada. The one person owns 20 percent of the property that the other person lives in full-time. She’s a 20 percent equity owner in the property. They are not married. That 20 percent equity owner lives in a foreign country.

If they rent that 20 percent share of the property to the partner — who they’re partners with but not legally married — would that exempt them, yes or no?

Hon. C. James: I think the first piece that I want to state is I’m not going to give tax information, as the Minister of Finance, specifically to an individual case. I think that’s really important.

I think individuals…. We are working on exactly the same letter that the member has and that the member from Prince George has as well. We are working through those pieces. There are so many unknowns around where the taxes are paid by the individuals. We don’t know that information. It wouldn’t be right for us to be asking that information, unless they were asking for tax information.

We’re quite happy to look at the situation. There may be a number of pieces that fit, but I don’t want to, as I said, jump on something where I don’t have all the information. But we have committed to making sure that we get the information for them.

Example 4 (Video 3): Extending over two lots

A. Weaver: I have a specific example I wish to offer the minister to seek some clarification. It’s a real-world example.

Let’s suppose that there is a person who happens to have a property that’s very old and lives in the riding of Oak Bay–Gordon Head. That property is a small house on a lot, but it’s actually two lots. One lot has the house; the other has an orchard that’s been in place in perpetuity. For the purpose of speculation tax, this might be considered as two properties. However, it’s only one property. It’s always been one property, and it will remain one property.

The question is: is the extra lot to be viewed, in this category here, as part of a whole property or not? Is there a means and ways that this person would be exempted by the administrator, and how would they be exempted by the administrator in this situation?

Hon. C. James: That would be an example where the individual could take it to the administrator and have it examined. I think the key around rules relating to the property is that the residential property — so if it’s the additional parcel, as the member describes — is used for the residence or for purposes ancillary to or in conjunction with the residence.

So as I said, I wouldn’t give the advice. That’s the job of the administrator. But that would be an example where they could take something to the administrator.

Example 5 (Video 3): Extending across two specified areas

A. Weaver: Thank you. That’s very helpful. I have a final question, and it’s relevant to the riding that I represent and part of the municipality that the minister represents.

There are properties in the capital region district where the actual property spans two municipalities. This is quite common along Foul Bay Road, in Oak Bay, where there are many houses that have part of the house in Oak Bay and part in Victoria. I suspect, without going through all of this, that there may exist properties in the province of British Columbia that actually span a jurisdiction that’s in and a jurisdiction that’s out. How would those be treated, if they do exist? And would the administrator automatically treat them in the in or out district?

Hon. C. James: We had a little bit of this discussion earlier. We found one property in the province, in the areas for the speculation tax, that spans inside and outside.

If a portion is inside, then they will be taxed — or subject to the speculation tax. I shouldn’t say they’ll be taxed, because they may have an exemption for other reasons. But it’ll be included as part of the speculation tax.

A. Weaver: Would the component of the property that’s subject to the speculation tax be the percentage of the lot that’s in the property or the total lot? Why I ask that? Let’s suppose there’s a 12-acre parcel of which 100 square metres is in taxation and the rest is not. Would they be collectively subject to the taxation? Again, these are not examples that I know of, but I know of them in Oak Bay–Victoria, as I’m sure the minister does. But there may be some that we’ll find out about.

Hon. C. James: Again, we found one property that fits that example. It will be the case that if a portion of the property is in, the entire property is subject to the speculation tax. But again, we think that this will be a very rare example. We found one. I don’t expect that there will be other examples.

Example 6 (Video 4): Couple – one in Kelowna, the other in Vancouver

A. Weaver: I have three personal stories I’d like to read and see if I can get the minister’s response. The first concerns a UBC professor I have been in touch with who has, most recently, been teaching at the Okanagan campus in Kelowna. They’ve had a home there since 2013, but they have a condo in Vancouver. His wife is teaching at the Okanagan campus, but he’s now teaching at UBC. They’re both UBC professors, but UBC has two campuses, one in the Okanagan and one at UBC in Vancouver. So he teaches in Vancouver; she teaches in the Okanagan.

He was teaching in the Okanagan. He was hit by the city of Vancouver’s empty homes tax last year and has since moved his primary residence to Vancouver as part of it. So now his primary residence is Vancouver to avoid the Vancouver vacancy tax, and his wife is still teaching at UBC Okanagan. His wife spends much of her time at UBC Okanagan.

My question to the minister is this. Can you confirm that this couple would be exempt because of the commuter marriage exemption that we’re discussing, when this fellow’s wife spends a good deal of time in Kelowna for work purposes?

Hon. C. James: Again, I’ll always put the caveat around: based on the information that’s here…. I certainly encourage people to make sure they phone the tax department and talk to the tax department to get the specifics. But on the information that the member has provided, yes, it appears that if one is working in the other place and one residence is the principal residence of the spouse, yes, they would qualify.

Example 7 (Video 4): Couple – live in North Saanich, work & rent in Vancouver

A. Weaver: Thank you. That’s very helpful.

This one’s a little more complex. And that was my understanding as well. I do appreciate hearing the confirmation, subject to the caveats, of course. They’re, of course, subject to caveats.

Another example is…. This one is very interesting. A couple that I know have been in touch with me. They own a house in North Saanich, which is in the covered regions of the capital regional district. They live in the house on weekends. That’s the only house they own. It is in North Saanich. However, they both work in Vancouver, and they rent a property in Vancouver during the week, although they live in North Saanich. This is relatively common these days in Victoria, where people cannot afford to actually own in Vancouver, so they live in the North Saanich area. They take the ferry on Monday to Vancouver. They work there, and they come back on the weekends. They plan to live permanently there, in North Saanich.

My question is: are they eligible for an exemption in this regard?

Hon. C. James: Again, based on the information provided, it would appear that they would be subject to the tax because it wouldn’t be their principal residence. The home in North Saanich would not be their principal residence. It’s not where they’re spending most of their time, so it does appear that they would be subject to the tax.

But I want to make sure that I’m clear on the caveat that everybody has some additional information, and when people talk to the tax department, they often provide further information that a person wasn’t sharing with an individual when they were talking to them. I would encourage people to make sure that they phone, for those kinds of examples, to make sure that they get the information from the tax department.

Example 8 (Video 4): Live in Surrey, work in Vancouver

A. Weaver: I very much appreciate that. I’m not trying to trap the minister at all. I’m trying to get some clarification and some advice that we can actually provide to these people who are rightfully concerned. Members of the opposition have been doing exactly the same thing. We do understand, of course, that the minister cannot provide tax advice.

It’s a bit odd asking questions in this marriage section, but people have asked us how marriage relates to this. This is a complex tax bill, and where people fit in with their individual cases is quite difficult.

The final example here is another woman. Again, she’s not covered under the commuter marriage, I don’t think. However, it’s odd, so maybe we could get kind of a general sense of the minister’s thinking on this issue.

This is an example of a woman who lives with her ailing mother in a family home in Surrey. So she lives in Surrey, her mother is ailing, and she lives there with her. But the woman actually works in Vancouver. She doesn’t want to take the tunnel, along with the member for Surrey–White Rock, so she has a condo in Vancouver, where she works during the week.

She owns the condo, and she also lives in the family home that she owns with her mother in Surrey. They’re clearly not married, but there clearly is a kind of commuter relationship there.

I’m wondering whether she could be exempt if she rented the family home to her mother? Is there a temporary exemption for something like that? I don’t know how this plays out.

Hon. C. James: With the caveat — I think that’s really important to state. If the individual works in Vancouver and has the Vancouver condo as her principal residence, for example, then her mother would be considered a non-arm’s-length tenant. She doesn’t have to rent; she can live in the house. She would not be paying the speculation tax. But again, lots of caveats around that to make sure it’s based on the principal residence — how much time she’s spending between the two places as well.

A. Weaver: Again, I don’t want to ask the minister to give tax or advice on buying or selling property, but I do think it’s important that we have this discussion and make it available to people so as to hear the kind of thinking of where things are going. The reason why I say this is that this particular person, also the condo that I mentioned in downtown Vancouver, is subject to a strata with a no-rental clause in it. So it gets even more complex there.

Unfortunately, this woman is selling her condo in downtown Vancouver. What I would like to get confirmed is that in fact there is place an exemption for 2018 and 2019 for any strata unit that has a no-rental clause in place. So rash decisions about putting a condo on for sale, when the condo is in a strata unit that has a no-rental clause, are not being forced by this legislation.

Hon. C. James: The member is correct. There is a two-year exemption for condos and stratas that have a requirement that you cannot rent the place out.

A. Weaver: I just want to thank the minister — this is very, very helpful — and the opposition for asking these questions. These are important issues, and having these answers on record is going to be very helpful.

Example 9 (Video 5): Strata accommodation properties & Oak Bay Beach Hotel

A. Weaver: On section 27, we’re talking here about strata accommodation properties. I’m wondering if the minister could please give the members here an idea, an estimate, of what type of properties these are, with some examples?

Hon. C. James: Strata accommodation properties that are classed as residential under the Assessment Act would be strata accommodation property short-term rentals, hotels, strata hotel accommodation that has been classed as class 1 or partially class 1 or partially class 6.

These hotels, a number of years ago, were given favourable property tax treatment, for example, to encourage the construction of these short-term occupancy time-shares, hotels.

I guess a way of describing it would be a cross between a strata complex and a hotel — that’s kind of a description — made up of individual strata lots that are pooled together for the purpose of being rented. That’s, I think, kind of the best description I could give.

A. Weaver: I can give some examples, then. Oak Bay Beach Hotel, for example, is a hotel in my riding that has a long history as a hotel, but it’s actually strata units that are rented out through a property rental agreement, and the zoning actually precludes any other use.

There are others in the minister’s own riding. Some are zoned tourist commercial. There are others in the province of British Columbia. In the tourist commercial zoning, for example, which some are zoned as, you actually have restrictions put on by your municipality, and those restrictions actually limit the ability for you to rent more than six months. So I agree. I think we’re on the same page as to what units are there.

My question, then. I understand that there’s no problem for the next two years — well, through 2019, because 2018 is exempt, as well, for these properties. My concern is: what is government’s intent for afterwards?

These properties are significant economic drivers in the region. Oak Bay Beach Hotel, for example, is one of the single biggest suppliers of property tax to the municipality of Oak Bay. They have very little commercial property in the riding, as well as in other jurisdictions. I’m sure there are, in my friend’s riding in Kelowna, tourism commercial properties that have similar zoning, as well.

Hon. C. James: The member, I’m sure, knows this, but the commercial portion is already not classed as residential, so therefore isn’t covered anyway because it’s often class 6 property.

I think the further review around how we deal with these properties is really the time that we gave, in this act, for two years. It gives an opportunity for discussions with the municipalities, with the property owners, etc., to find a long-term solution. This gives us the opportunity to have those kinds of conversations.

Example 10 (Video 6): Medical Exemption in Nanaimo

A. Weaver: With respect to section 33, I have a personal story I’d like to relate to the minister. I’m not asking for tax advice. I’m recommending people go to the information that the minister provided yesterday on the record, and that will be here. But I’ll just give a sense of the intent, because this is an illustrative example.

This is an example of a couple who recently bought a second home in Nanaimo. They live on a small island nearby with their daughter, and they spend several days a week at the Nanaimo property. They bought it so they could be closer to the hospital. They’re elderly.

The property is worth less than $400,000. It’s a $300,000 property. They don’t want to rent it out, because they’re elderly, they’re concerned about medical issues, and they want to go there if they have to be there for medical reasons. Right now, they only have to be there on and off, but they might have to be there at any time for a more extended period of time.

I’m just asking if the minister could please confirm to me that the couple is not covered by the medical exemption, yet they are covered by the fact that the property is $300,000, which is under the $400,000 exemption.

The idea here is that while they have bought a property to go every now and again, it’s still not being used full-time. They’re not needing it full-time. But because it is

The idea here is that while they have bought a property to go to every now and again, it’s still not being used full-time. They’re not needing it full-time, but because it is under $400,000, they are exempt.

I’m wondering if the minister, without providing tax advice, could confirm that the general spirit of this would be that they would have an exemption because it’s under $400,000, but they’re not eligible for the medical exemption.

Hon. C. James: I appreciate that I must have said it often enough. Based on the information that the member provided — recognizing that the individual should make sure they get tax information from the taxes people — yes, if it’s less than $400,000 there, that will cover it, and they will not pay the speculation tax. As the member says, from the information he has given, they wouldn’t appear to be covered under the illness, but they would be covered under the $400,000.

UVic gets major boost in student housing

Today I had the honour of participating in an announcement at the University of Victoria outlining a major new investment in student housing via the BC Student Housing Loan Program. Two new buildings will be built on the campus to house 782 students (a net increase of 630 student homes). In addition, a new dining hall and multipurpose space will be incorporated into the new space.

I’m thrilled to see this student housing project move forward at the University of Victoria. Not only will this new project provide critically needed on-campus housing, but the new buildings will also be constructed to the Passive House standard. Both UVic and the Province are demonstrating leadership in innovative low-carbon housing solutions, and I look forward to similar projects rolling out throughout British Columbia in the months ahead.

Today’s announcement is not only good for students, but also for individuals and families trying to rent across Greater Victoria. We have one of the lowest rental vacancy rates in the province, and because of a lack of on-campus housing, students are competing with everyone else in Victoria for the same scarce rental units. By better meeting the needs of students with on-campus housing, this project will help ease the pressure in the rental market.

Below is the text of the brief speech I gave at the event.

Text of Speech

I’m delighted to be here today to welcome the news that UVic will see the construction of 782 new homes for students (of which 620 are net new).

I’m delighted to be here today to welcome the news that UVic will see the construction of 782 new homes for students (of which 620 are net new).

UVic students have been in desperate need of more affordable, on-campus housing for years now.

Ever since I was first elected as an MLA in 2013 I’ve been calling on government to take steps to create more student housing at UVic, as well as other universities across BC.

I’m thrilled that the BC NDP government is listening and making increased student housing a reality.

Today’s announcement is not only good for students, but also for individuals and families trying to rent across Greater Victoria.

As I’m sure everyone here knows, we have one of the lowest rental vacancy rates in the province.

And because of a lack of on-campus housing, students are competing with everyone else in Victoria for the same scarce rental units.

By better meeting the needs of students with on-campus housing, this project will help ease some of that pressure in the rental market.

It will free up rental units in the rest of the city for everyone else who is looking for a place to call home.

I find this project particularly exciting not only because it will provide critically-needed on-campus housing, but also because the new buildings will be constructed to the Passive House standard.

The Passive House standard is a world-leading standard for energy efficiency. This is exactly the type of innovative approach that we need to take in dealing with the climate crisis.

In every new building, in each new piece of infrastructure, we have an opportunity to reduce our emissions and build the type of communities we want.

UVic and the province are demonstrating leadership in developing innovative low-carbon housing solutions. In fact, every capital project government is involved in should be seen through the lens of low carbon innovation.

I offer my sincere thanks and congratulations to both UVic and the government of BC for demonstrating leadership in dealing with our affordability crisis while at the same time recognizing the opportunity for innovation in the low carbon 21st century economy.

Introducing amendments to the speculation and vacancy tax

In the legislature today the Minister of Finance introduced a motion to send a number of amendments to committee stage for Bill 45 – 2018: Budget Measures Implementation (Speculation and Vacancy Tax) Act. These amendments match the three amendments that I put on the order papers although they were drafted by independent legislative drafters. The reason why government needed to do this was to ensure that my amendments were not ruled out of order by the Clerk. Amendments can be ruled out of order if they incur a cost on government.

Below I reproduce (in text and video) my brief remarks in response to the Minister’s motion. I was inappropriately cut off by the Speaker. The motion was a debatable motion and I should have been given 30 minutes to address it. The speaker was reacting to Mike Farnworth, the BC NDP House Leader, who stood up and was gesticulating to me and the speaker that the the motion wasn’t debatable. He was wrong. But you can’t challenge a speaker’s ruling.

Text of Speech

A. Weaver: Just a few words briefly on this motion. I’m pleased, obviously, to rise and take my place in the debate on this. The motion to move the amendments to the speculation and vacancy tax act.

For procedural reasons, government had to table these amendments. You’ll see some amendments I put in on the order paper as well. But the amendments that government is tabling reflect the agreement that we were able to reach with government on this tax a few weeks ago. I’m pleased to be supporting moving them to committee today. These amendments do three things — the three things as promised. Again, on the order paper, you will see three amendments that I put in that are virtually identical. But for procedural reasons, government is introducing these amendments.

The first is that mayors from affected municipalities will be consulted annually by the Minister of Finance on how the tax is affecting their communities, with metrics that are being developed. Over the past number of months, I’ve consistently raised the need for local governments to have a more significant role in determining what happens in their communities. The annual review of the tax with mayors will give communities a clear channel to making the case, based on evidence, for how the tax should apply to their communities and whether they should be excluded.

The minister will also be required to report the results of the annual review to cabinet to make a decision on whether the tax should continue to be applied in each of the specified areas. While I would have preferred for local governments to have the ability to opt out automatically, this is a compromise position that I feel I can support and my colleagues can support as well.

The second amendment requires that revenue raised by the tax will be used for housing initiatives within the region it came from. This is also important — that local communities directly benefit from the tax raised so that it is not viewed as a tax grab by government that rolls the moneys into provincial coffers to be lost thereafter. There needs to be a clear impact on the communities because the justification for the speculation tax is, of course, that there’s an externality, a social cost, that we’re asking people in British Columbia and elsewhere to internalize through the application of the speculation and vacancy tax.

The third amendment equalizes rates for Canadians and British Columbians. It brings the rate for Canadians down from 1 percent to 0.5 percent. Now, this is a very big change. Back in the spring, when this tax first came out, it was 2 percent for other Canadians.

Here after many, many months of working with government to come to razor-focus this tax to exactly this intent and purposes, it’s very reassuring to see that the rate has come down to 0.5 percent.

I believe fundamentally that from a fairness perspective, we should not be penalizing Canadians by making them pay higher rates just because they happen to live in another province. We are one country. I feel that as one country, we need to treat our citizens equally across that country.

In addition to these amendments, government has made a number of small changes in the legislation that go a long way to limiting the unfair impacts of this tax on Canadian homeowners who aren’t speculators.

Since it was first introduced in the budget, I’ve been hearing scores of cases that I’ve been bringing to government over the past eight months from people who are not speculators and who should not be facing the tax, as well as other examples where the speculation tax shouldn’t apply.

Deputy Speaker: Thank you, Member.

A. Weaver: My understanding, hon. Speaker, is on a motion, I am able to deliver a full 30 minutes.

Deputy Speaker: Member, this is purely a procedural motion. This allows the amendments to be placed before the House for debate. Not at this time.

A. Weaver: Is this not a debatable motion, hon. Speaker?

Deputy Speaker: Not at this time. This is a motion to refer.

Motion approved.

Video of Speech

Latest Posts

Recent Comments

- on The Paris Agreement is in trouble: UNFCCC needs to ratchet up their climate efforts

- on The Paris Agreement is in trouble: UNFCCC needs to ratchet up their climate efforts

- on How can BC’s environmental organizations be more effective?

- on How can BC’s environmental organizations be more effective?

- on How can BC’s environmental organizations be more effective?